Determining the value of a small, privately owned business is a challenging task. To do so properly requires skill, a lot of research, analysis, and a strong understanding of the business being valued and the space in which it operates. Unfortunately, the topic of business valuation is far too large to teach in a blog post. Yet what I am able to do is provide a review of the three main business valuation approaches and conceptually how they work and when they can be used.

Call for a free consultation:(602) 410 – 0802

They are:

– the Income Approach

– the Market Approach

– the Asset Approach

Each approach views a business from a different perspective in order to measure value; each has relative strengths and weaknesses, and there are circumstances when one may be more useful than another. An important initial distinction between the approaches is that the Income and Market Approaches work from the income statement; they are driven by a company’s ability to generate revenue and profit. Said another way, the Income and Market Approaches measure performance. The Asset Approach, however, is driven by the target’s balance sheet, where value is a measure of company assets after subtracting liabilities.

More explanation about each one of the approaches is below.

The Income Approach: This is generally the most involved valuation approach of all, as it requires a lot of research, analysis, and judgment calls about how a company will perform in the future, what reinvestment needs will be, and so forth. This is also considered by many valuation professionals to be the most desirable valuation approach. This is because it ultimately provides a value based on those traits that are specific to the company; it is referred to by some as an Intrinsic Valuation because company value is determined by those characteristics that are specific and inherent to the company, i.e. how much money will this company generate and how risky is it?

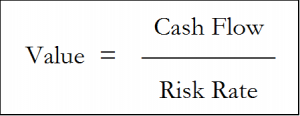

The approach determines value by calculating the present value of all future cash flows. What does that actually mean, you ask? So let’s say a company will make money in the future (at least we hope). First, we need to come up with estimates of how much cash flow a company will generate next year, and the year after, and so on. Once we have the estimates, we need to decide how uncertain we are that those cash flows will actually happen; we quantify our uncertainty by means of a risk rate. The higher the level of uncertainty, the greater the risk rate. This is intuitive, as all it is really saying is as risk increases, we demand an ever greater return on our investment. Said another way, the riskier we view this company’s future cash flows, the less value they have to us today. The rate is referred to as a discount rate or cap rate, depending on the situation. The relationship between cash flow and risk rate, in its simplest form, can be seen in the formula below:

This formula illustrates the basic relationship between cash flow and risk: as cash flows get bigger, value increases; as risk gets smaller, value also increases. And vice versa.

Thus, the use of this approach involves determining what a business’ cash flows will be in coming years and applying the correct risk rate to them. While this sounds simple, it is often quite complex and involved.

In order to use the Income Approach to value a company, we need to make a few determinations:

– How far into the future do we expect the company to generate earnings?

– What do we expect cash flows to be over that time period?

What level of risk will we associate with those cash flows?

Each one of the three preceding points requires serious consideration; the middle point, what will cash flows be, is typically going to be the most time consuming step. It requires making decisions about how large the market space will be, how much market share the target company can get, what will profits be, and how much will the expected growth cost?

Shortcomings of the Income Approach include the fact that it is complex to perform; it can be very time consuming and requires strong technical skills in working with accounting records and financial statements. And it requires estimating a company’s future performance, a subjective exercise in the hypothetical.

This approach is useful for valuing companies that are expected to continue operating into the foreseeable future. As mentioned previously, this method is heavily favored by many professionals because it is based directly on the future cash flows and risk rate of the target company. And generally, the greater our level of confidence in our projected cash flows, the greater our level of confidence in the value conclusion.

The Market Approach: This approach uses information about other companies to help determine business value. It does this by comparing the target company to a group of companies that are considered comparable, i.e. companies that are similar in terms of industry, size, operating characteristics, and so forth. The approach also requires that the comparable companies provide a sufficient level of information about their performance and details about transactions in their ownership interests. So in order to use this method, you need a group of comparable companies and you need to determine where your target company fits, in terms of performance and desirability, along the spectrum of values that the comparable group presents to you.

The approach will result in a multiple that must be applied to some performance measure for your target company. For example, the result may say that, based on how your company compares to the group, your target company should be valued at a multiple of 0.8 of annual revenue, or 3 times discretionary earnings, or 5 times EBITDA, etc.

This approach can be particularly strong if you have a large group of comparable companies to work with and the company you are valuing is mature and substantially similar to the comparable companies. But there can be challenges to using this approach. For example, expected growth rates are hugely important in company valuation, yet we generally do not know what the expected growth rates were for the comparable company transactions. So if your target company is experiencing above-average growth, it can be tricky to know where it should place against the group of comparable companies.

Another drawback of this approach relates to the ability to identify comparable companies. If you are trying to a value a company that is doing something unique, it can be quite a challenge to form a group of comparable companies that is large enough to provide a meaningful reference point. If the group is small and of low quality, in terms of similarity to your target company, the indication of value that this approach will provide will probably also be of low quality.

Some people refer to this as a “relative” approach to valuing a company because it determines value based upon how the target company looks relative to a group of similar companies.

This approach, like the Income Approach, is also best used when valuing a going concern, i.e. a company that will continue operating into the foreseeable future.

The Asset Approach: As the name suggests, this valuation approach focuses on the value of a company’s assets. The fundamental difference between this approach and the other two approaches (the Income and Market Approaches) is that this approach is based on the balance sheet whereas the other approaches are based on the income statement. Said directly, the asset approach looks at a company and asks how much the assets are worth today: this involves determining the value of both tangible and intangible assets and subtracting the company’s liabilities.

This approach is often used to value a company that is not expected to continue operating in the future. One way of thinking of this approach is to ask the question, “if this company were to shut its doors, how much would be left after we sold its assets and paid its debts?”

This approach can be used to value a going concern, but if used to do so, it is only to set the floor value. In this situation, the Asset Approach value of a company helps us know if the company is worth more dead or alive. For example, if the asset approach suggests the company is worth $1 million, but the income and market approaches suggest it is worth only $800,000, then the company would in fact be worth more dead than alive. If this were the case, ownership would need to evaluate the possibility of closing the company, liquidating assets and returning the $1 million in proceeds to stakeholders.

In closing: It is important to know that each one of the three approaches reviewed above has a number of different methods under its umbrella that can be used to determine company value; a method is the specific manner or technique by which one calculates a value. For example, under the Income Approach, one could choose the Single Period Capitalization Method, or the Multiple Period Discounting Method, depending on the situation at hand. And within a particular method, there are multiple options for determining the required variables in the valuation formula, e.g. the Ibbotson Build-Up approach or Duff & Phelps to determine a risk rate. The Market and Asset Approaches are similar in that they also have multiple methods and numerous finer points to resolve in their application. I mention these details not to confuse readers, but simply to point out that there is a lot more to valuing a company that we have not reviewed here.

So once you’ve used the approach(es) to determine value, what’s next? Some professionals may reach a final conclusion of value based upon the result of only one single approach, while others may use a weighted average of two or more approaches depending on their level of confidence in each value indication. There are no set rules on how to weight the value indications from the different approaches; it is entirely up to the individual and will be based upon their own experience and judgement.

Ultimately, my intent in writing this review was simply to inform readers of what the three valuation approaches are and how they work in concept. I’m hopeful that I have done that for you.

If you have questions, comments or things you’d like to add, please feel free to get in touch with me or comment below. I’d be happy to hear from you.

Call for a free consultation:(602) 410 – 0802